Column

Accounting & Tax Treatment of Office Interior and Furniture Costs in Vietnam

2026/03/24

オフィス関連

ベトナム関連

マネジメント

This article explains the key accounting and tax treatment points that those who suddenly bear this important responsibility should keep in mind —

clearly explained by Mr. Jitsuhara, CEO of I-GLOCAL, the largest Japanese accounting firm in Vietnam.

~ How costs are spread over time, and key points for confident budget planning ~

|

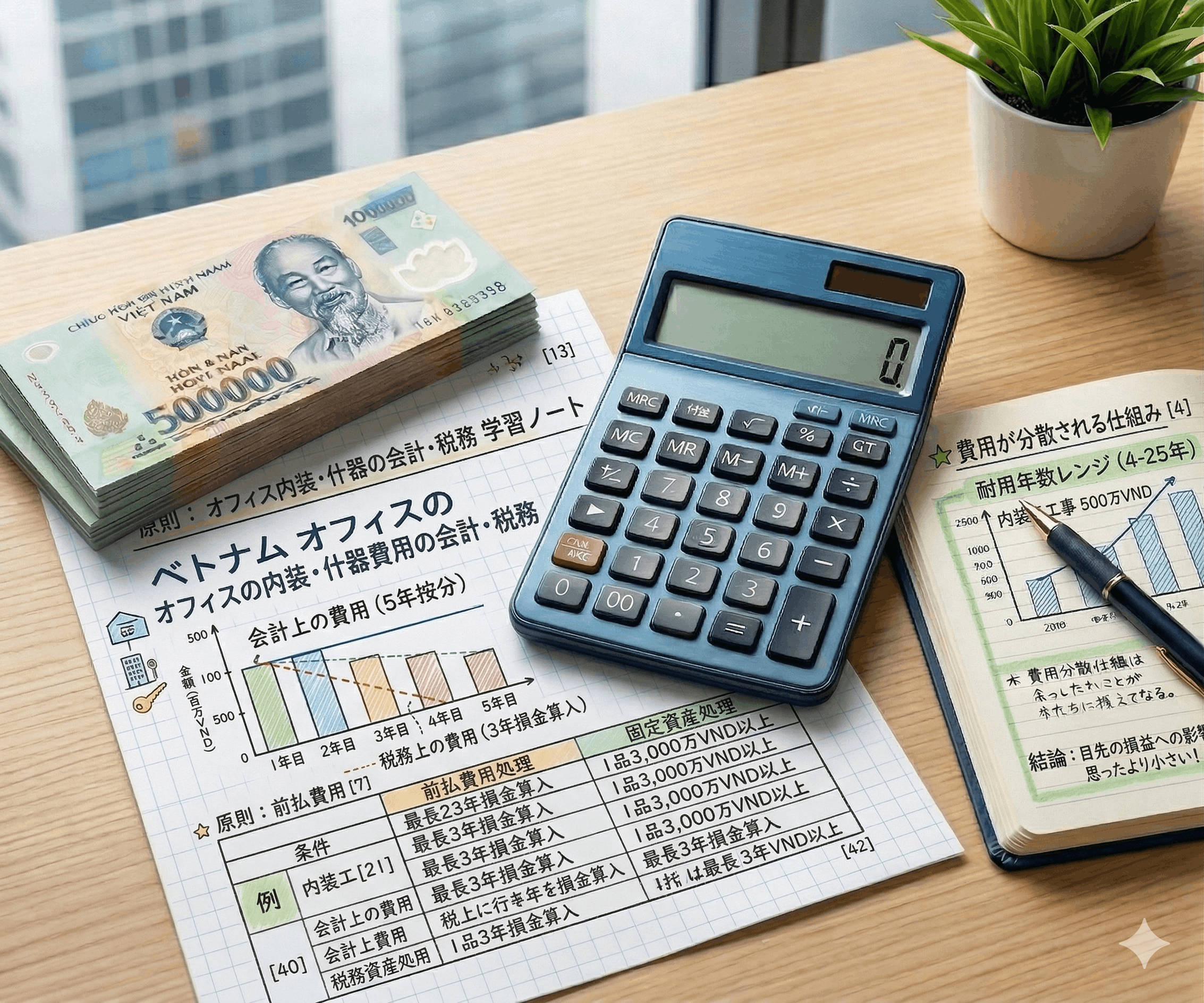

💡 Even if you invest heavily in interior renovation, the accounting expense is spread over several years. For example, a ¥5 million renovation spread over 5 years means only ¥1 million per year is expensed. The impact on near-term profit & loss is smaller than you might think. |

When opening or renovating an office in Vietnam, interior renovation costs and furniture purchases can amount to significant sums. However, by properly understanding how these costs are treated from an accounting and tax perspective, you can spread costs appropriately over time and reduce the impact on near-term profit and loss. This column explains — assuming a leased office — how interior renovation costs and furniture costs are treated in an easy-to-understand manner.

1. Treatment of Renovation Costs

General Rule: Recorded as Prepaid Expenses (Cost Spreading)

Interior renovation costs for a leased office do not qualify as fixed assets, since the building is not owned. As a general rule, they are recorded as “prepaid expenses (deferred assets)” and spread over the lease term or expected useful life.

|

【Example】Renovation cost: ¥5 million / Lease term: 5 years Accounting: Spread over 5 years → ¥1 million expensed per year Tax: Deducted over max. 3 years → approx. ¥1.67 million deducted per year Since the tax deduction comes sooner than accounting expense, the tax benefit arrives earlier. |

Exception: Recording as Fixed Assets

Work that meets all of the following conditions may be recorded as a fixed asset and depreciated over its useful life.

- ◆ Constitutes an upgrade (improvement in productivity, quality, utility, etc.)

- ◆ Can be identified as an independent asset (machinery, equipment, etc.)

- ◆ Meets the 3 conditions for fixed assets (see below)

When recorded as a fixed asset, depreciation is applied within the following useful life ranges (per Circular 45/2013/TT-BTC). Note that interior finishes such as partitions, ceilings, and floors generally cannot be independently recorded as fixed assets.

| Type of Work / Equipment | Useful Life Range | Reference |

|---|---|---|

| Electrical equipment (power, lighting, etc.) | 7–15 years | Circular 45/2013/TT-BTC |

| Air conditioning equipment | 6–15 years | Circular 45/2013/TT-BTC |

| Elevators and lifting equipment | 6–10 years | Circular 45/2013/TT-BTC |

| Communications, IT, and electronic equipment | 3–15 years | Circular 45/2013/TT-BTC |

Note: Recording as a fixed asset requires itemized invoices or contracts. If an invoice states “interior renovation (lump sum),” the prepaid expense / cost-spreading treatment applies.

|

💡 In practice, most renovation costs are treated as prepaid expenses. In Vietnam, “interior renovation (lump sum)” invoices are common, making individual asset identification difficult. The prepaid expense approach is dominant in practice. Only independently identifiable items — such as electrical or air conditioning installations — are recorded as fixed assets. |

2. Treatment of Furniture Costs

Three Conditions for Fixed Asset Classification

Furniture such as desks and chairs may be recorded as fixed assets if all three of the following conditions are met.

- ◆ Future economic benefits are expected

- ◆ The asset will be used for more than one year

- ◆ Acquisition cost is 30 million VND (approx. ¥180,000) or more per item

Furniture that does not meet all three conditions is treated as a prepaid expense (max. 3 years for tax). The assessment is made per item — totals cannot be aggregated. Most ordinary office chairs and desks fall below the per-unit threshold, so prepaid expense or immediate expensing is most common in practice.

|

💡 Fixed asset classification for furniture is the exception, not the rule. The threshold is assessed per item regardless of how many are purchased together. Most ordinary office chairs and desks fall below 30 million VND per item, so prepaid expense or immediate expensing is the most common outcome. Only high-value furniture or large equipment exceeding the per-item threshold qualifies as a fixed asset. |

Spreading Period When Treated as Prepaid Expense

The spreading period may be set freely based on a “reasonable expected useful life.” In practice, most companies use the 3-year tax maximum for simplicity. While periods of up to 5–7 years are theoretically permissible, 3–5 years is the realistic range.

Reference: Typical Useful Lives for Furniture

| Type of Furniture | Useful Life Range | Reference |

|---|---|---|

| Chairs, desks, tables, shelves, curtains, etc. | 4–25 years | Circular 45/2013/TT-BTC |

| TVs, projectors, etc. | 3–15 years | Circular 45/2013/TT-BTC |

| Computers | 3–8 years | Circular 45/2013/TT-BTC |

3. Summary

| Treated as Prepaid Expense | Treated as Fixed Asset | |

|---|---|---|

| Renovation Costs |

▶ General rule Accounting: spread over lease term Tax: deducted over max. 3 years |

▶ Upgrade + independent asset (3 conditions met) Fixed asset → depreciated over useful life (Electrical: 7–15 yrs, A/C: 6–15 yrs, etc.) |

| Furniture Costs |

▶ Does not meet 3 conditions Accounting: spread over expected useful life Tax: max. 3 years; small items expensed immediately |

▶ Meets 3 conditions per item (≥30M VND) Fixed asset → depreciated over useful life ※ Uncommon in practice |

With a 5-year lease, both renovation and furniture costs can generally be spread over 5 years for accounting purposes. Even with a large upfront investment, the annual accounting expense is smaller than expected. Since tax deductions are allowed over a maximum of 3 years, the tax benefit arrives sooner — an added advantage.

We hope this gives you the confidence to create your ideal office. If you are uncertain about how to treat any costs, please feel free to consult a specialist.

Writer

Takayuki Jitsuhara

- Introduce yourself

- Takayuki Jitsuhara Partner, I-GLOCAL CO., LTD. Certified Public Accountant (Vietnam & U.S.) Professional Profile A native of Yokosuka City, Japan, Graduated from the Faculty of Engineering at Kobe University. He joined I-GLOCAL in 2009 and relocated to Vietnam the same year. Since then, he has dedicated his career to consulting for Japanese companies, specializing in market entry strategies and post-entry management and operations within the Vietnamese market.

New Topics

Top 5 popular articles